Storm hits. Roof takes damage. Claim gets filed. An adjuster shows up, writes an estimate, and you receive a number that feels… off. That’s where hail damage claim supplements: what carriers miss in their scope becomes the most important part of your entire claim. Because here’s the truth most initial insurance estimates are incomplete. Not slightly off. Not “good enough.” Incomplete.

And if you don’t correct that scope, you don’t get paid for the full repair. Simple as that. In areas like McAllen, where sudden hailstorms can impact entire neighborhoods in minutes, homeowners often assume the first estimate is final. It’s not. It’s just the starting point. Let’s break down exactly what’s happening and how to take control of your claim.

What Is a Hail Damage Claim Supplement?

A supplement is not a redo. It’s a correction. A refinement. A strategic adjustment based on real findings. It’s the process of identifying missing, under-scoped, or incorrectly priced items in the original insurance estimate and submitting them for additional compensation.

Think of it this way:

- Initial estimate = surface-level evaluation

- Supplement = full reconstruction of reality

Supplements are not rare. They’re expected. Contractors rely on them daily. Public adjusters build claims around them. Insurance carriers review them constantly. And when done correctly, they transform a lowball estimate into a realistic settlement.

Why Insurance Carriers Miss So Much in Their Scope

It’s not always about bad intent. But it is about limitations.

Speed Over Accuracy

After a major storm, adjusters are flooded with claims. Their schedule tightens. Inspections get shorter.

They’re under pressure to:

- Move quickly

- Close files

- Keep claim flow moving

Speed becomes the priority. Accuracy takes a back seat.

Surface-Level Inspections

Not every roof gets a full walk-through.

Adjusters may:

- Inspect from the ground

- Check only accessible slopes

- Skip steep or complex sections

That means damage goes unnoticed. Especially the kind that costs the most to fix.

Cost Containment

Insurance carriers operate on controlled payouts. One of the most effective ways to manage costs? Start with a limited scope. Not necessarily incorrect. Just incomplete. And that’s where hail damage claim supplements: what carriers miss in their scope enters the picture.

Lack of Trade-Level Detail

Roofing systems are layered systems. Each component matters.

But if someone isn’t deeply familiar with installation practices, they may overlook:

- Starter shingles

- Drip edge

- Flashing transitions

- Ventilation balancing

Miss these, and the estimate falls short.

The Role of Xactimate in Hail Damage Claim Supplements

This is where the numbers get real.

What Is Xactimate?

Xactimate is the industry-standard estimating platform used across the insurance and restoration industries.

It breaks repairs into:

- Material costs

- Labor costs

- Equipment charges

- Regional pricing

Every component has a code. Every cost is tracked.

Why Xactimate Accuracy Matters

Small errors create large gaps. If one line item is missing, it doesn’t just remove a cost it removes the entire scope tied to it. In McAllen, localized pricing is critical. Labor costs, material availability, and regional demand all affect the final estimate. Using incorrect pricing? That alone can undercut your claim.

How Professionals Use Xactimate

Experts don’t just input numbers. They build narratives.

A strong Xactimate estimate:

- Mirrors real construction processes

- Includes all necessary layers

- Accounts for access difficulty

- Reflects local pricing trends

This is how supplements gain traction.

Commonly Missed Line Items in Hail Damage Claims

This is where claims lose money.

| Category | Line Item | Impact |

| Roofing | Tear-off & disposal | High |

| Roofing | Starter shingles | High |

| Roofing | Ridge caps | Medium |

| Flashing | Step flashing | High |

| Ventilation | Ridge vents | Medium |

| Code | Compliance upgrades | High |

Miss enough of these, and the estimate drops far below reality.

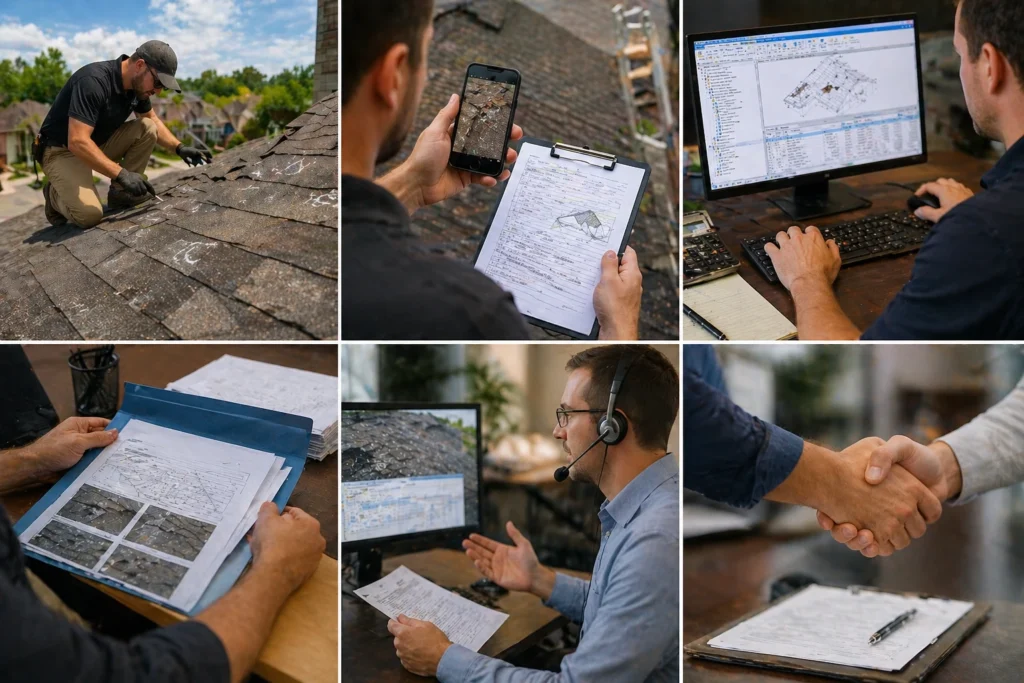

The Supplement Process Step-by-Step

Step 1 – Detailed Inspection

Every slope. Every detail. No shortcuts.

Step 2 – Documentation

Photos, notes, measurements. Clear and organized.

Step 3 – Xactimate Estimate

Line-by-line reconstruction of the true scope.

Step 4 – Submission

All findings presented to the carrier.

Step 5 – Negotiation

Back-and-forth. Justification matters.

Step 6 – Approval

Scope updated. Payment increased.

Real-World Scenario: Initial Scope vs. Supplemented Claim

Initial Claim

- Basic roof replacement

- Missing key components

Payout: $12,500

Supplemented Claim

- Full system replacement

- Added flashing, ventilation, code upgrades

Final Payout: $21,800

Same storm. Completely different result.

How Poor Documentation Weakens Your Supplement

Weak documentation kills strong claims.

Avoid:

- Blurry photos

- Missing angles

- No written explanation

Strong documentation builds leverage.

Advanced Xactimate Strategies That Increase Claim Value

Use Local Pricing

McAllen costs vary. Your estimate should reflect that.

Layer Line Items

Roof systems are multi-layered. Price them that way.

Identify Hidden Damage

Look beyond the surface. That’s where value is.

Justify Code Upgrades

Without documentation, upgrades get denied.

What Happens If Your Claim Gets Denied?

Sometimes the issue isn’t underpayment it’s denial.

Understanding What to Do If Your Hail Claim Was Denied in Texas becomes critical at this stage, because many denied claims can still be reopened, supplemented, and successfully paid when proper documentation and scope corrections are submitted.

Why a Public Adjuster Changes the Outcome

Representation matters.

- Insurance adjuster → protects the carrier

- Public adjuster → protects you

That difference shows up in the numbers.

The Financial Impact of Missing Scope

Even small omissions add up:

- Flashing: $500–$1,500

- Ventilation: $800–$2,000

- Underlayment: $1,000+

Miss multiple items, and you’re leaving thousands on the table.

A Note on Complexity in Claims

Insurance claims, much like concepts in advanced fields such as epistemology, rely heavily on how knowledge is interpreted, validated, and presented. The more structured and evidence-based your claim is, the stronger your position becomes during review and negotiation.

Final Thoughts: Precision Wins Claims

This isn’t about luck. It’s about detail. Strategy. Execution. Most claims don’t fail because damage isn’t covered. They fail because it isn’t properly scoped.

That’s what hail damage claim supplements: what carriers miss in their scope is all about. If your estimate feels incomplete, it probably is. Fix the scope. Strengthen your documentation. Push for accuracy. Because the difference isn’t small. It’s everything.

FAQs

A supplement is a revision to your insurance estimate that adds missing or underpaid items to reflect the true cost of repairs.

Adjusters work quickly after storms and may overlook details, leading to incomplete scopes.

Depending on what was missed, supplements can add thousands of dollars to your final settlement.

Yes, most carriers require Xactimate-formatted estimates because it’s the industry standard.

Yes, supplements are often submitted during repairs when hidden damage is discovered.

Flashing, ventilation, underlayment, and code upgrades are frequently overlooked.

It typically takes 1–3 weeks, depending on documentation quality and carrier response time.

You can provide additional documentation, request a reinspection, or escalate the claim.

A public adjuster can improve accuracy and negotiation outcomes, often increasing your payout.

No, approval depends on proper documentation, justification, and alignment with policy coverage.